Rules for Offering California Small Business Health Insurance

Overview

If you’ve got fewer than 100 employees in your company and you’d like to offer employee benefits, then you should know about the guidelines the State of California has established for group health insurance for small businesses. These guidelines implement the Affordable Care Act (ACA, or Obama Care) requirements. All of the insurance companies (Aetna, Anthem, Kaiser, etc.) must follow these rules. Read the PDF below and you’ll learn about:

- Summary

- The Way Rates are Calculated

- Eligible Small Employer

- Eligible Employee

- Important Requirement: Employer Contribution

- Important Requirement: Employee Participation

- Employer “Shared Responsibility” Penalty for Small Groups

- Small Business Health Insurance Tax Credit

- Summary and Market Considerations

Rules for California Small Business Health Insurance (PDF version)

California Small Business Health Insurance Requirements

Are employers required to offer health insurance?

The Affordable Care Act requires small business owners in California with more than 50 employees to contribute to a group health insurance plan for W-2 employees, or pay a penalty. Employers must contribute or pay a minimum of 50 percent of the least expensive health insurance plan offered by the insurance company.

Let us help you sort it out

While the ACA has standardized many aspects of group health insurance, there is still a lot of variation that allows you to set up the plans that will best meet the needs of your company and your employees. Contact us now and we can help you (800)746-0045.

The following is a concise description of small business health insurance.

June 2025

This is a summary of the rules that govern small group health insurance plans in California. The rules described in this document include the “Obama Care” (Affordable Care Act, ACA) guidelines and are current and up-to-date as of June 2025. These rules apply to companies with up to 100 employees. If you offer a group health insurance plan – or you’re thinking of offering a plan to your employees – give us a call at (800) 746-0045 and we can become your agent/broker/advisor. We’re experts and we can help you.

Regulations

All medical insurance companies must follow guidelines established by the Federal government and the State of California. Some of these rules may not make sense but we’ll try to explain the purpose of the rules in this summary. If you want to check out the source regulations see California Health and Safety Code (HSC) Section 1357.500; and the California Insurance Code (CIC) Section 10753 and CIC section 10755. The Federal regulations are 42 US Code Section 18024; Affordable Care Act Section 1304; and 45 CFR Section 155.20.

Recent Changes

California law (California Code Title 24, Ch. 38, Sec. 10 Stats. 2019) continues to impose a penalty of up to 2.5% of income on any Californian who doesn’t have medical insurance. California also continues to forbid association plans with SB 1375 and

DMHC All Plan Letter 19-024. Legislators reasoned that association plans would weaken California’s strong market for small businesses.

Standardized Benefits

Health insurance companies must offer the identical plans to small businesses with 1 to 100 employees – just because you only have a few employees doesn’t mean that you get worse plans. You can select any plan an insurance company offers. Also, insurance companies allow you to offer many different plans to your employees. Some employees can be on an HMO and others can enroll on a PPO – all allowed.

Standardized Rates

The rate or monthly cost (politely called a “premium” in insurance speak) is based on the location of the business and the exact date of birth of the employee AND the date of birth for each dependent. So, a spouse age 49 will cost more than one age 48. See the chart below:

The Way Rates are Calculated

Rates based on each employee’s & dependent’s exact age

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Employee | Spouse | Child | Child | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0-14 | 0-14 | 0-14 | 0-14 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 15 | 15 | 15 | 15 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 16 | 16 | 16 | 16 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 17 | 17 | 17 | 17 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 18 | 18 | 18 | 18 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 19 | 19 | 19 | 19 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 20 | 20 | 20 | 20 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 21 | 21 | 21 | 21 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 22 | 22 | 22 | 22 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 23 | 23 | 23 | 23 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 24 | 24 | 24 | 24 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 25 | 25 | 25 | 25 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 65 | 65 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

California has 19 different rating regions, many of which include multiple counties. Los Angeles is so large that it’s split into two separate regions (15 & 16) and sometimes rates are cheaper for a business located in Pasadena than in Downtown LA.

One thing to note is that once you set up your plan; the rates are fixed for 12 months, which means that when someone has a birthday their rate won’t change until your group’s plan renews the following year.

No Medical Underwriting

This means that no matter the health characteristics of your employees and their dependent spouses and children, you will not be charged more for their coverage. Prior to the ACA or “Obama Care”, everyone had to answer medical questions and rates could increase for pre-existing medical conditions. No longer. You and your employees get the same rate if you’re running triathlons or if you have one foot in the grave. (See California Insurance Code Section 10753.08) 12 Month Rate Guarantee. California state law mandates that the rate you pay for health insurance stays the same for an entire 12 month period – of course if you add or delete employees from the plan the amount you pay will change. However, an insurance company can’t just raise your rates after a few months. Also, as noted in the section on “standardized rates,” rates won’t change when someone has a birthday and moves into a new age category. After a year, when the health plan renews, all of the enrollees move into a new age category and receive the rate for their new age.

Guaranteed Renewal

Decades ago an insurance company could decline to renew your group health insurance plan if an employee or dependent had a major illness or injury. That was blatantly unfair and the government put an end to it years ago. The ACA forbids insurance companies from asking questions about an enrollee’s medical condition. They must offer coverage and renew that coverage to every small business, regardless of any pre-existing medical conditions. So, if someone in your group gets really sick; don’t worry. It won’t affect the rate you pay.

Some variation

California State Insurance Regulations give insurance companies some leeway on a few items and each company may have slightly different criteria. These differences may allow your company to qualify for coverage with one insurance company but not qualify with another insurance company. You should work with a knowledgeable, licensed health insurance agent to help you find the best coverage at the lowest price. Of course we recommend BenefitsCafe.com because we’ve taken the time to do the research and write this document and we like helping people. Best of all there is no charge for our services. Give us a call today at (800) 746-0045.

Minimum Essential Benefits

Small businesses that offer health insurance coverage must offer plans that have 10 minimum essential benefits. These include:

- Outpatient care you receive in a doctor’s office and not in the hospital

- Evaluation and treatment in the emergency room

- Inpatient care after you’ve been admitted to a hospital

- Care before and after your baby is born

- Treatment that includes psychotherapy and counseling for mental health and substance use

- Prescription medicine

- Physical and occupational therapy, speech-language pathology, psychiatric rehabilitation and other services to help you recover from an injury, disability or chronic condition

- Laboratory tests

- Preventive services such as screenings, counseling and vaccinations

- Pediatric services for children under age 19 that includes dental and vision care

Source: HealthCare.com: What Marketplace Health Insurance Plans Cover

Eligible Small Employer

Federal and State laws require that an employer have at least 1 but not more than 100 employees to qualify as a small business for purposes of group health insurance. Brand new businesses have a difficult time qualifying for coverage. To address this problem, the law says that a small company must have employed at least one non-owner W-2 employee for 50% of the preceding calendar year or 50% of the preceding quarter. So, for example, if a business wants to start a group health plan April 1st, which is the start of the 2nd quarter, then the company must have had at least one W-2 employee no later than February 14th of the same year – this is the midway point of the 1st quarter. Small businesses must submit their most recent Quarterly Wage Statement (Form DE9C) to an insurance company when they apply for coverage. Insurance companies use the DE9C as a roster of employees to determine eligibility. As a practical matter, newly formed start-ups can submit 2-4 weeks of payroll records in lieu of the DE9C; but insurance companies can decline to offer coverage to groups that don’t meet the “50% of the preceding quarter” requirement.

Metal Tiers

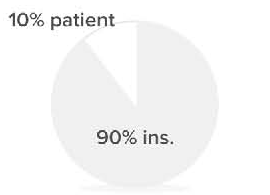

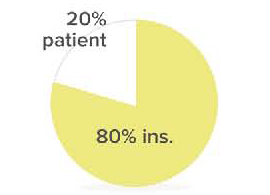

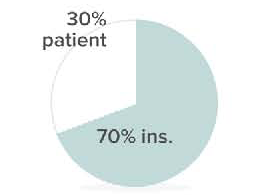

The ACA requires all insurance companies to identify each plan by its actuarial value (AV). To simplify this already too complicated concept, the ACA created “metal tiers” that correspond to an actuarial value. In this way, people can easily determine that a platinum plan will pay more for services than a gold, silver or bronze plan. See the chart below:

The ACA Uses Metallic Levels to Compare Plan Benefits

| Platinum | Gold | Silver | Bronze | |

|---|---|---|---|---|

| Percent of medical expenses paid: Insurance plan vs. patient pays (Co-insurance) | 10% patient 90% insurance |

20% patient 80% insurance |

30% patient 70%insurance |

40% patient 60%insurance |

| Deductible | None or Low | Low | Moderate | High |

| Co-payments | Low | Low | Moderate | High |

| Out-of-pocket limits | Low | Low | Moderate | High |

By using the metal tier one can reasonably assume to pay less for medical services on a higher metal tier plan. However, the metal tier does NOT indicate the extensiveness of the provider network of doctors and hospitals. So, you can have a very rich benefit platinum plan that costs relatively little. This happens when that plan only includes a few in-network doctors and hospitals.

Minimum Value of Insurance Plans

The ACA put an end to skimpy benefit plans – ones that paid very little for medical services and left employees facing financial ruin. All small group health insurance plans must have a minimum actuarial value of 60%. The actuarial value (AV) is “the percentage of total average costs for benefits that a plan covers.” A plan with 60% AV would require the member to pay 40% of the cost for medical services and the insurance company would pay 60%.

Eligible Employee

An employee must be a “W-2” eligible employee, i.e. someone from whom you withhold payroll ( FICA) taxes. An employer-employee relationship exists between the company and the workers. In contrast, a “1099” person who works for you is not an eligible employee. A 1099 person is an independent contractor who works for you and can work for other employers. No employer-employee relationship exists. 1099’rs aren’t eligible for your group health insurance plan.

California state law considers any W-2 employee who averages 30 hours or more of work per week over the course of a month to be eligible for the group health insurance plan. This means that you can’t be more restrictive and, for example, only offer coverage to employees who work 32 hours per week – such a restriction would violate California State law (see: California Health and Safety Code Section 1357.500(c)(1)) On the other hand, you can be less restrictive and offer coverage to part-time employees who work as few as 20 hours per week.

Owner-Only Businesses Don’t Qualify

California State Law defines a small employer as one with a “a bona fide employer-employee relationship.” The law requires that a small business have at least one non-owner W-2 employee. This also means that an owner’s spouse who works in the company won’t qualify the business for small group coverage.

Important Requirement: Employer Contribution

Employer Contribution

California health insurance companies require that an employer contribute at least 50 percent of the employee only monthly cost or “premium.” So, for example, if the monthly cost for one employee (not including dependents) is $500, then the employer must pay at least $250. Some insurance companies allow a lower employer contribution amount using a “defined contribution” arrangement.

Insurers that allow employers to contribute as little as $80/ employee/month:

• Aetna

Insurers that allow employers to contribute as little as $100/ employee/month:

- Anthem Blue Cross

- Blue Shield

- Health Net

- United Health Care

Insurers that require employers to contribute 50% of the least expensive plan offered:

- Covered California for Small Business

- CalChoice

- Kaiser

These minimum requirements may change but they are accurate as of June 2025.

The employer contribution is important for insurance companies because it ensures that a large number of employees will enroll, not just the unhealthy ones. The employer contribution is also important for employees because it determines the amount the employees will pay for their medical insurance. It’s like a teeter-totter: the more the employer pays, the less the employees pay. If employees are asked to pay too much for their coverage relative to their income, they will likely decline to enroll. This causes a problem for the second requirement: Employee Participation.

California Small Group Health Insurance Employee Participation Requirements

| Insurance Company | Group Size (number of Enrolled EEs) |

Employee Participation Requirement |

|---|---|---|

| Aetna* | 1-4 EEs | 60% |

| 5-100 EEs | 25% | |

| Anthem Blue Cross* | 1-4 EEs | 65% |

| 5-100 EEs | 25% | |

| Blue Shield of California* | 1-100 EEs | 65% |

| 5-100 EEs | 25% | |

| CaliforniaChoice | 1-2 EEs | 100% |

| 3-100 EEs | 70% | |

| Covered CA for Small Business (SHOP) | 1-100 EEs | 70% |

| Health Net* | 1-4 EEs | 70% |

| 5-100 EEs | 25% | |

| Kaiser | 1-100 EEs | 50% |

| United Health Care* | 1-4 EEs | 60% |

| 5-100 EEs | 25% |

* Note: The companies with an asterisk (*) show the “relaxed” participation requirements and these percentages may change. If you’re concerned that not enough employees will enroll; then call BenefitsCafe.com, (800)746-0045, for the latest guidelines. We can help you figure out a strategy that may work for you and your employees.

Important Requirement: Employee Participation

Employee Participation

Most California medical insurance companies require that at least 60 to 70 percent of the eligible employees actually enroll in the medical insurance plan offered by the employer. Again, this ensures that the majority of the employees – healthy and unhealthy – enroll in your small group medical insurance plan. In technical insurance-speak, this prevents “adverse selection,” where people more prone to using medical care sign up for coverage. Adverse selection causes the premium to increase for everyone, so the participation requirement prevents this problem.

The Affordable Care Act, or Obama Care, dramatically changed the participation guidelines for California health insurance companies. The table above shows the minimum percentage of employees who must enroll in a group health plan. Note that you can exempt some employees from the calculation; see the next section on “Participation Waivers and Declines.”

Participation Waivers and Declines. The guidelines for California small group health insurance allow an employer to omit certain employees from the participation calculation. Specifically, an insurance company allows employees to “waive” coverage if they obtain health insurance through a different source:

- As a dependent through a spouse or parent’s employer’s group health plan, or

- Individually through Medicare (usually for seniors age 65 or older), or

- Individually through Medicaid (MediCal in California which is for low income people).

These are valid “waivers” and the insurance company omits the employee from the calculation of eligible employees. On the other hand, some insurance companies will consider employees to have “declined” coverage, if the employee has:

- No health insurance coverage, or

- Individual health insurance plan through Covered California or an individual “off-exchange” plan.

These are “declines” and they DO count against the participation requirement. (Note: Anthem Blue Cross, Blue Shield, Health Net and United Health Care treat individual coverage as a waiver and not a decline. This may help some employers qualify for coverage with these insurance companies.)

Here is an example. Imagine a company with 10 full time, eligible W-2 employees. One employee’s husband works for the telephone company and she is covered as a dependent on her husband’s plan. That’s a waiver. Another employee is covered by his parents through his mom’s employer. This is another valid waiver. A third employee is covered by his wife’s individual plan obtained through Covered California. This is a decline. In this example, we have 2 valid waivers which makes 8 eligible employees and we have 7 employees enrolling in the group plan. 7 divided by 8 is 87% (usually you round down.) This is above the 70% minimum and the group qualifies. However, if two additional employees decided that they didn’t want any health insurance and declined the group coverage, then we would only have 5 enrolling employees of the 8 eligible employees. Five divided by 8 is 62% and we wouldn’t be able to enroll with an insurance company that required 70% participation.

Can an employer pay 100% of health insurance for employees?

Yes, an employer can pay 100% of the cost of medical insurance for employees, and many do. Employers who find it difficult to attract and retain good employees often pay 100% of the premium for medical insurance for employees. Some employers even pay some or all of the cost for dependent coverage (spouse and children). If you are trying to figure out how much you should contribute to your employees medical insurance, give us a call (800)746-0045 and we can help guide you.

Affordable Group Coverage

With few exceptions, the ACA requires everyone in the United States to have health insurance. The government limits the amount that they expect people to pay for employer sponsored health insurance to 8.50% of household income in 2025. Employers won’t know an employee’s “household income”, which may include income from a spouse working for a different employer. So, the IRS has a “safe harbor” test for employers: as long as the employee’s share (or contribution) for self-only medical insurance is less than 8.39% of the employee’s W-2 wage, the employer is considered to offer “affordable” coverage.

Active Status with the California Secretary of State

To qualify for small business medical insurance; a company must be listed with “active” status in the California Secretary of State’s directory of business entities. Most insurance companies require businesses applying for new coverage to submit a copy of the “Statement of Information” which is included in the directory.

The ACA places a “pay or play” penalty on employers with 50 or more full time “equivalent” employees (i.e., 2 part-timers equal one “full time equivalent” or “FTE.”) The government refers to this as “shared responsibility” because employers share the responsibility of paying for coverage with their employees. Employers with fewer than 50 FTEs face no penalty if they don’t sponsor a group health insurance plan or if the coverage is unaffordable as described above. All businesses with 50 or more FTEs face a penalty if they fail to offer “minimum essential coverage” that is affordable to their full time employees. See these IRS Employer Shared Responsibility guidelines.

Reporting to the IRS for Employers with Fewer than 50 FTEs.

If you have fewer than 50 full time equivalent employees (FTEs); then you won’t need to submit anything to the IRS or to your employees to stay in compliance with the ACA – the insurance company will do that for you1. Insurance companies will complete and send Forms 1094-B and 1095-B on your behalf. The 1095-B is like a W-2 but for medical insurance, where the W-2 reports wages earned, the 1095-B reports medical insurance coverage. Employees use form 1095-B to show that they and their dependents had “minimum essential coverage” for some or all of the tax year. The 1094-B Form is the cover or “transmittal” report for the 1095-B form.

1 This assumes that your group medical plan is “fully insured” which means that you pay an insurance company to handle everything (that’s the type of group medical insurance that we’ve discussed in this article.) If your plan is “self-insured” or “self-funded” then you will need to submit tax forms as if you’ve got 50 or more FTEs – it’s much more complicated.

Reporting to the IRS for Employers with 50 or more FTEs.

Companies with 50 or more FTEs must report to the IRS and issue forms to employees (Form 1094-C and 1095-C). To do this, an employer must keep track of all employees on a monthly basis and determine whether the employee is:

- eligible and enrolled;

- eligible and not enrolled; or

- not eligible for the group medical plan.

Employers also need to determine whether the amount the employee pays for the coverage is “affordable” which is a simple calculation using the “safe harbor” test mentioned earlier. As with anything surrounding taxes, things can get complicated. You need to work with your accountant and/or attorney. We help our clients locate consultants who specialize in this and/ or recommend software to assist employers. We don’t give tax advice –those guys and gals get paid a lot more than we do and have much more expertise in tax law – but if Benefits Cafe is your agent we will work with your tax professionals to help you comply with the law.

Favorable Tax Treatment

One important note for an employer is that the IRS and the State of California give extremely favorable tax treatment to employer paid health insurance premium: the amount the employer pays is a fully tax deductible business expense. Employer-sponsored health insurance is also great tax-wise for employees because it is non-taxable compensation to the employee.

See the chart “Why it’s Better to Buy Health Insurance Through your Employer” on page 8 of this document.

Employees are NOT eligible for Covered California Subsidies when they have access to coverage through an employer:

While this is not actually a rule of small group health insurance, it is good to know. Many people who apply for individual health insurance with Covered California (California’s ACA “exchange”) often apply for an “ Advanced Premium Tax Credit.” The tax credit lowers the monthly cost or “premium” of the individual plan. The tax credit can also lower the copayments for very low income people. The government figures that if your employer subsidizes your health insurance coverage then tax payers shouldn’t.

Small Business Health Insurance Tax Credit

The ACA gives a financial incentive to certain small businesses that offer affordable health insurance to their employees. In order to qualify for the tax credit (which is much more valuable than a tax deduction), a business must:

- Have fewer than 25 full-time equivalent employees (i.e., 2 part-timers equals 1 full time equivalent)

- Have the average wages of employees to be less than $65,000/year

(you exclude the wages of owners and their family members who work in the business) - Contribute at least 50% of the cost of employee-only coverage – this shouldn’t be a problem since most California health insurance companies require a minimum 50% employer contribution.

- Purchase group health insurance through the state at Covered California for Small Business (Formerly SHOP). BenefitsCafe.com (800) 746-0045 can help you set this up.

While that is the criteria, it is a bit misleading. The full tax credit is 50% of the employer paid premium, which is potentially a lot of money. The difficulty is that for a small business to qualify for the full 50% tax credit, the employer must have:

1. Fewer than 10 full-time equivalent employees (i.e., 2 part-timers equals 1 full time equivalent)

AND

2. The average wages must be $32,000 per year or less.

As the average wages paid in a company increase; the tax credit decreases “exponentially.” Which, if you remember your high school or college calculus, means that the tax credit decreases rapidly as wages increase slightly. An average wage of $32,000 may go a long way in other parts of the country, but in California few employers can attract and retain employees by paying this little. $32,000/year is about $15.38/hour. California’s minimum wage is $16.50/hour in 2025. Another not-so-good feature of the tax credit is that you can only receive it for two consecutive years. So, if you sign up in 2025 and you qualify in subsequent years; you’ll only get the credit for two years. Still, the small business health insurance tax credit may defray some of the cost of providing medical insurance to your employees.

You can estimate the amount of credit that your company may qualify for by visiting the Federal Government Small Business

Tax Credit Calculator. Also, the IRS has good information on their page: Small Business Health Care Tax Credit for Small Employers. Finally, you should consult a tax professional for additional information.

Summary and Market Considerations

In this document we’ve summarized the most important rules that govern small group health insurance in California. The rules create a level playing field and ensure that the insurance companies treat everyone fairly. We’re lucky that many insurance companies offer coverage in California’s small group market including: Aetna, Anthem Blue Cross, Blue Shield of California, Health Net, Kaiser, and United Health Care. We also have two “exchanges” that enable small businesses to offer more than one insurance company at the same time: Covered California for Small Business (formerly SHOP), which is run by the State of California and offers tax credits to certain small businesses; and CalChoice, a privately-owned “exchange” that offers coverage from United Healthcare, Anthem, Health Net and Kaiser. With so many options, small businesses have a good chance of finding coverage that is affordable. Give BenefitsCafe.com a call at (800) 746-0045 and we can help you.

Why it’s Better for an Employee to buy Health Insurance Through their Employer

| Buying Individual Health Insurance Through Covered California | Buying Group Health Insurance Through Your Employer | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Employee’s Monthly Salary | $2,000 | $2,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Medical Insurance Premium* | $0 | $200 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Taxable Salary | $2,000 | $1,800 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Employee Payroll Dedications |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Federal Income Tax @ 15% | $300 | $270 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| FICA (Social Security & Medicare) @ 7.65% | $153 | $138 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| State Income Tax @ 4% | $80 | $72 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Medical Insurance Premium | $200 | $0 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Take-Home Pay | $1,267 | $1,320 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Increase in Take-Home Pay Per Month: $53/mo. ($1,320 – $1,267)

Increase in Take-Home Per Year: $636 ($53 x 12 months)

* Section 125 of the Tax Code allows employees to pay their portion of health insurance premium “pre-tax” and legally avoid State and Federal income taxes and FICA taxes (Social Security and Medicare.) Individual coverage is “after-tax” and subject to these taxes. In this example, the savings is greater than three months’ medical insurance premium ($636 / $200 = 3+ months’ savings on health insurance premium.)

Written by Bruce Jugan who is the President of BenefitsCafe.com, the online home of Professional Benefits & Insurance Services. We’re a family owned insurance agency, founded in 1970, and we specialize in employee benefits. Give us a call, 800 746-0045.